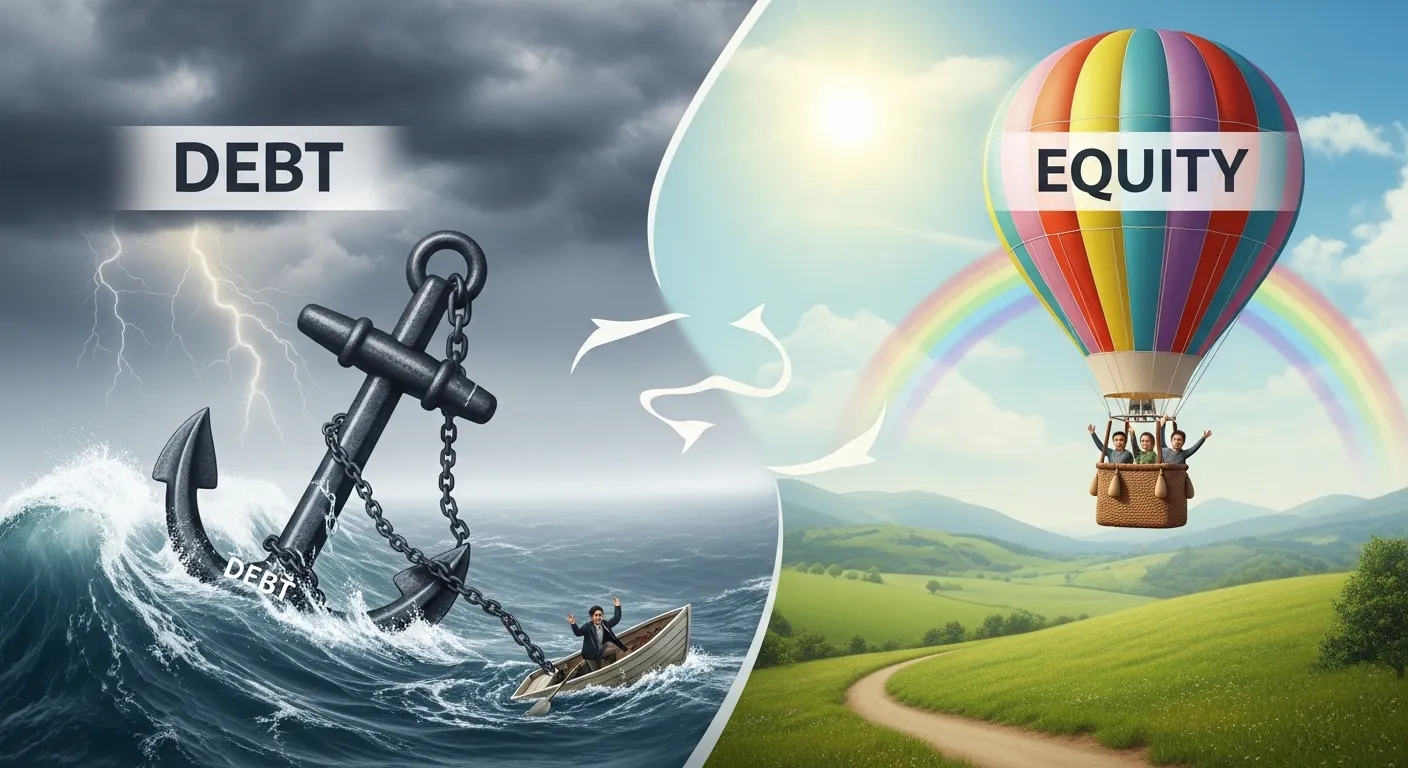

Imagine you are starting a new business, and you need funds to expand. You have two main options: borrowing money from a bank or inviting investors to buy a share of your company. This is where understanding the difference between debt and equity becomes essential. Debt involves borrowing money that must be repaid with interest, while equity represents ownership in the company in exchange for capital. Many new entrepreneurs confuse debt and equity, but knowing the difference helps in making strategic financial decisions. In this article, we will explore the difference between debt and equity, their advantages, risks, and how they impact your business and investment decisions.

Pronunciation

- Debt: US /det/, UK /det/

- Equity: US /ˈek.wɪ.ti/, UK /ˈek.wɪ.ti/

Linking Hook: Now that we understand what debt and equity mean, let’s explore their differences in detail.

Difference Between Debt and Equity

1. Ownership

- Debt: Lender does not get ownership of the company.

- Example 1: Bank gives a loan; owner retains full control.

- Example 2: Bonds issued to raise funds without giving ownership.

- Equity: Investors become part-owners.

- Example 1: Selling shares to raise capital.

- Example 2: Venture capital investment in exchange for equity.

2. Repayment Obligation

- Debt: Must be repaid with interest.

- Example 1: Monthly loan installments to the bank.

- Example 2: Corporate bonds with fixed maturity.

- Equity: No repayment obligation; investors earn dividends.

- Example 1: Shareholders receive dividends if profits exist.

- Example 2: Equity investors wait for stock appreciation.

3. Risk

- Debt: Lower risk for lenders; company may default.

- Example 1: Bank expects regular payments regardless of profit.

- Example 2: Bondholders get fixed interest.

- Equity: Higher risk for investors; return depends on company success.

- Example 1: Startup investors may lose all investment.

- Example 2: Share value may fluctuate in the stock market.

4. Cost

- Debt: Interest payments are fixed and often tax-deductible.

- Example 1: Business pays 8% annual interest on loan.

- Example 2: Tax deduction reduces net cost of borrowing.

- Equity: Cost is potentially higher as investors expect returns via dividends or profit share.

- Example 1: Paying 20% of profit as dividends.

- Example 2: Sharing ownership reduces future earnings per owner.

5. Control

- Debt: Borrower retains full control.

- Example 1: Bank cannot interfere in business decisions.

- Example 2: Loan agreement has limited covenants.

- Equity: Investors may demand decision-making rights.

- Example 1: Venture capitalists may require board seats.

- Example 2: Shareholders vote on major business issues.

6. Term

- Debt: Fixed term, usually with a maturity date.

- Example 1: Five-year business loan.

- Example 2: Ten-year corporate bond.

- Equity: No maturity; investment is long-term.

- Example 1: Common stock remains until sold.

- Example 2: Founders maintain shares indefinitely.

7. Impact on Cash Flow

- Debt: Regular repayment affects cash flow.

- Example 1: Loan installments reduce monthly cash.

- Example 2: Interest payments reduce available working capital.

- Equity: No regular outflow; dividends optional.

- Example 1: Dividends paid only if profitable.

- Example 2: Retained earnings stay in the company.

8. Tax Treatment

- Debt: Interest is usually tax-deductible.

- Example 1: Reduces taxable profit for companies.

- Example 2: Interest expense benefits cash flow.

- Equity: Dividends are not tax-deductible.

- Example 1: Paid from after-tax profit.

- Example 2: Increases shareholder tax obligations.

9. Financial Statements Impact

- Debt: Appears as a liability on the balance sheet.

- Example 1: Long-term loans listed under liabilities.

- Example 2: Interest expense shown on income statement.

- Equity: Appears under shareholder’s equity.

- Example 1: Common stock and retained earnings recorded.

- Example 2: Dividends reduce retained earnings.

10. Priority in Bankruptcy

- Debt: Lenders get repaid before equity holders.

- Example 1: Bank loans paid first.

- Example 2: Bondholders receive assets before shareholders.

- Equity: Last in line to receive any remaining assets.

- Example 1: Shareholders may get nothing if company fails.

- Example 2: Stockholders’ loss is risk of ownership.

Nature and Behaviour

- Debt: Predictable, contractual, lower risk for lender, limited impact on control.

- Equity: Uncertain, ownership-based, high risk/reward, potential influence on company decisions.

Why People Are Confused

Many confuse debt and equity because both raise capital, but one is a loan (debt) and the other is ownership (equity).

Table: Difference and Similarity

| Feature | Debt | Equity | Similarity |

| Ownership | None | Partial ownership | Both provide funds |

| Repayment | Required with interest | Not required; dividends optional | Can generate returns |

| Risk | Lower for lender | Higher for investor | Both involve financial risk |

| Control | Borrower retains control | Investors may influence decisions | Both affect business finances |

| Duration | Fixed-term | Long-term / indefinite | Both used for funding |

Which is Better in What Situation?

Debt is better for businesses with steady cash flow needing funds without giving up ownership. Equity is better for startups or companies seeking growth with high-risk tolerance, where repayment may be difficult. Choosing the right mix can optimize financial stability.

Use in Metaphors and Similes

- Debt: “The loan hung over him like a debt chain, restricting freedom.”

- Equity: “Equity in the company is like planting seeds—growth takes time and care.”

Connotative Meaning

- Debt: Neutral to negative, often implying obligation.

- Example: High debt can be stressful for businesses.

- Equity: Neutral to positive, implies investment and growth potential.

- Example: Equity investment fuels expansion.

Idioms or Proverbs

- “A fool and his money are soon parted” – relates to risky equity investments.

- “Neither a borrower nor a lender be” – relates to debt responsibility.

Literature Featuring the Keywords

- Rich Dad Poor Dad (Finance/Personal Growth, Robert Kiyosaki, 1997) – explains debt vs equity.

- The Intelligent Investor (Finance, Benjamin Graham, 1949) – covers equity investment principles.

Movies About the Keywords

- The Big Short (2015, USA) – explores debt markets and financial risk.

- Wall Street (1987, USA) – deals with equity investment and corporate finance.

FAQs

1. Is equity riskier than debt?

Yes, equity returns depend on company performance.

2. Can a company raise funds using both?

Yes, companies often use a mix for balance.

3. Which is cheaper, debt or equity?

Debt may be cheaper due to tax-deductible interest, but risk is higher for borrower.

4. Do investors get repaid like lenders?

No, investors earn dividends and capital gains, not guaranteed repayment.

5. What happens if a company fails?

Debt is repaid first; equity investors may lose all.

How Both Are Useful for Surroundings

Debt allows businesses to expand quickly without giving away ownership. Equity encourages investment in growth, innovation, and long-term economic development. Both strengthen financial ecosystems.

Final Words

Debt and equity are two sides of the funding coin. Entrepreneurs and investors must understand their differences to make smart financial decisions. Proper use ensures growth, sustainability, and balance between risk and control.

Conclusion

Debt and equity serve distinct purposes in finance. Debt provides predictable, contractual funding, while equity offers shared ownership with growth potential. Understanding the difference helps entrepreneurs raise capital efficiently, manage risk, and maintain control over business operations. Investors can also make informed decisions, balancing risk and reward. Clear knowledge of debt versus equity strengthens financial literacy and contributes to long-term business success, making it essential for both professionals and beginners.